Much has been discussed about the growth trajectory of NEVs and the potential growth trajectory of battery materials such as lithium, graphite, nickel, cobalt, rare earths and others. A potential sleeper in the conversation so far has been the notion that kerbside weight of electric vehicles is typically higher than it is for comparable internal combustion engine (ICS) vehicles. Auto producers, therefore, are forced to look more closely at reducing weight in the rest of the vehicle to compensate for the additional weight of the battery.

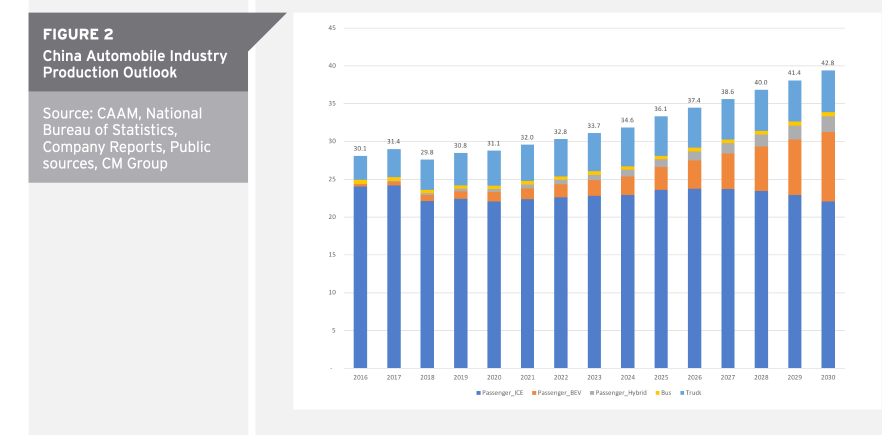

Over the period to 2030, China’s automotive sector is forecast to undergo a substantial transformation, shifting from ICEs toward New Energy Vehicles (NEVs). As materials of choice amongst China’s auto producers to reduce kerbside weight, both aluminium and magnesium appear well positioned to take advantage of the transformation. Despite the outlook for ICE vehicle numbers remaining flat, weight-savings could increase intensity of use and drive higher volumes of both materials.

CM has prepared detailed forecasts for both aluminium and magnesium usage in China’s automotive sector. A special report prepared for the International Aluminium Institute (IAI) is available for download. The report concludes a potential CAGR of 8.9% for primary Al consumption in the EV market.

CM’s work in the automotive sector covers developments in the global primary Mg sector, which the company has been analysing for over 20 years (CM Mg page here).

Over the longer-term, we believe the global automotive sector will be forced, through increasingly tight legislation, to significantly reduce emissions. The sector will gravitate naturally toward materials offering a genuine means to reduce kerbside weight from vehicles, one of which is magnesium. The metal is, in fact, an outstanding contender.

As the drive to reduce kerbside weight intensifies, both Mg and Al consumption is forecast to grow, regardless of whether the auto industry pursues internal combustion engines (ICE) or swings more aggressively to electric vehicles (EV). In both cases, vehicles will need to be lighter. Stronger demand and a more balanced supply base, we believe, will increase the attractiveness for these materials and drive strong growth over the long term.

The CM Group has a proven capability to conduct detailed market studies, supply demand analyses and a range of other specific, single scope studies in China as well as other South East Asian countries. CM’s project work regularly sees it’s teams on the ground in countries such as Indonesia, Malaysia, the Philippines, Myanmar and Vietnam. Our regional hubs in Singapore, Chengdu and Beijing reduce the need for lengthy field visits because we can deploy our specialist teams to target locations quickly and at low cost.